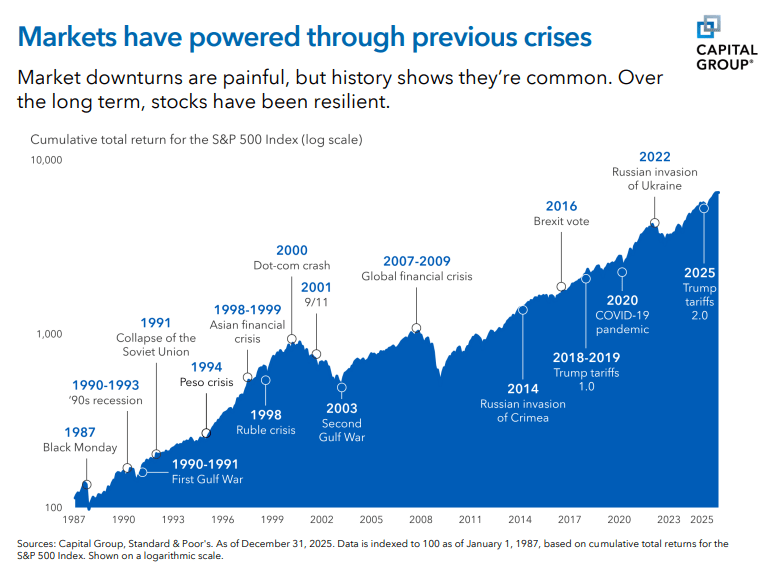

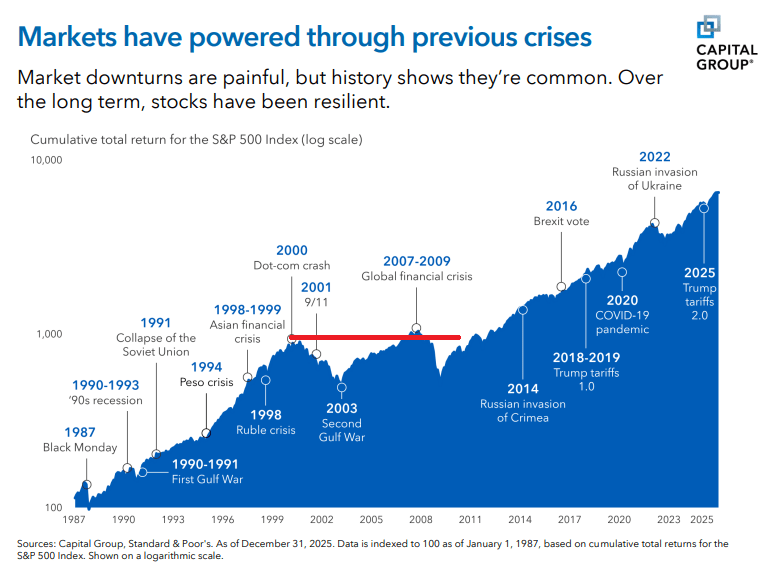

I want to open this article by sharing that, in the year since I started this blog, I haven’t shared a single post that hasn’t felt tone-deaf or insensitive to current events. Here we are a year later, and there still isn’t an appropriate time to discuss how our money is doing in light of the news without feeling a bit soulless. As difficult as things are in some parts of the world, one still needs to manage their finances, and that is where it is my job to remain focused. The current geopolitical conflict raises many concerns, and for investors, one of those concerns is what impact this all might have on the US stock market. A very timely chart came across my desk recently that was published by The Capital Group, a mutual fund company I partner with to offer college savings accounts at Northshore Wealth Management. It’s a chart that offers perspective on just how many crises and disruptive events have occurred in recent decades and the impact those have had or haven’t had on the S&P 500 Stock Index over the long term.

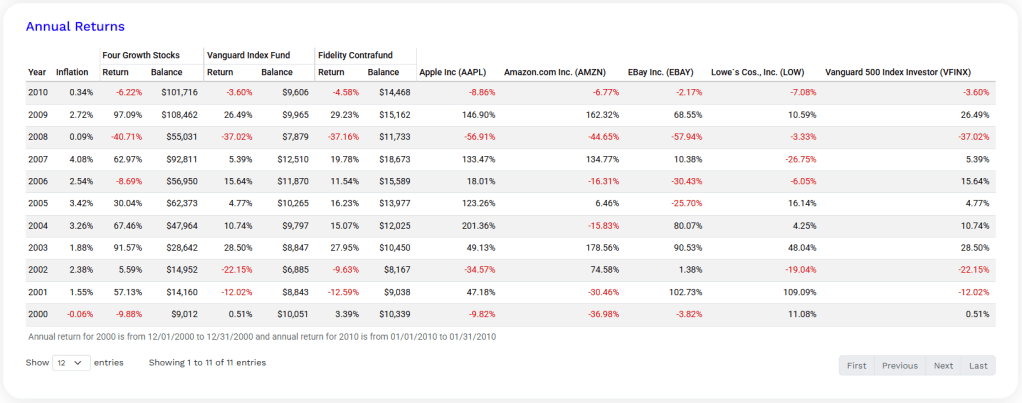

There is plenty to look at here, but while I was studying this chart, I noticed an entirely separate issue that this chart never intended to illustrate. If you look at this from a broader lens, it does a great job of illustrating one of the reasons I don’t endorse index investing as a growth strategy. Index investing has worked well for people over the last 15 years, but most of us need a good growth strategy to work for more than 15 years in order for us to build wealth. If you look closely, you’ll see this chart does a good job of illustrating what happened to index investors in the decade from 2000 to 2010. Nothing. Nothing happened for index investors in that decade. They earned nothing. And if you really check the dates, they actually lost money in that decade.

If you look at the scale of how much time we have to build wealth in our lifetime, a decade of missed growth is quite catastrophic. We don’t really begin earning money to invest until our early twenties, at best, and then most of us retire in our 60’s, which gives us about 40 years to achieve wealth. Imagine losing an entire quarter of your opportunity. But not everyone missed out on growth in that decade. Not everyone was an index investor like they are today. Today’s overwhelming popularity of index investing has me quite concerned. There is a lot that I agree with Warren Buffett on, and the truth is, he has been one of my greatest teachers over my lifetime, but I believe he did investors a disservice by telling them all to give up on aspiring to be anything better than completely helpless.

“Completely helpless” weren’t his exact words. People love to quote Buffett as saying, “Index investing is a sensible strategy for the average investor”. But that’s not the entire quote. He followed that by explaining that this is because the average investor “knows nothing,” and I equate the words “knows nothing” to “completely helpless”. If I were Warren, I would have pointed out that the average investor knows nothing and the average investor would be wise to do something to fix that, not just give up and resign themselves to helplessness. That is because the next time we experience a flat decade in the stock index, the helpless investor who doesn’t know what else to do might miss out on an entire quarter or their life’s potential to grow wealth. Sorry, Warren, but I don’t agree that’s the best solution for investors.

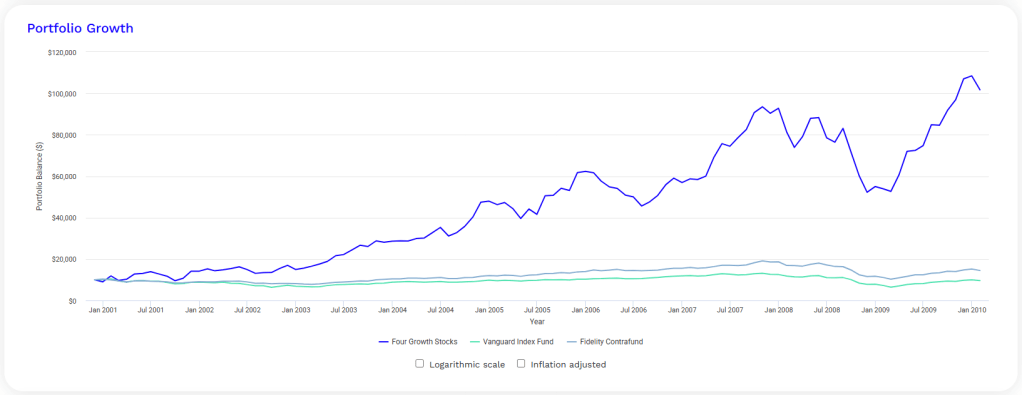

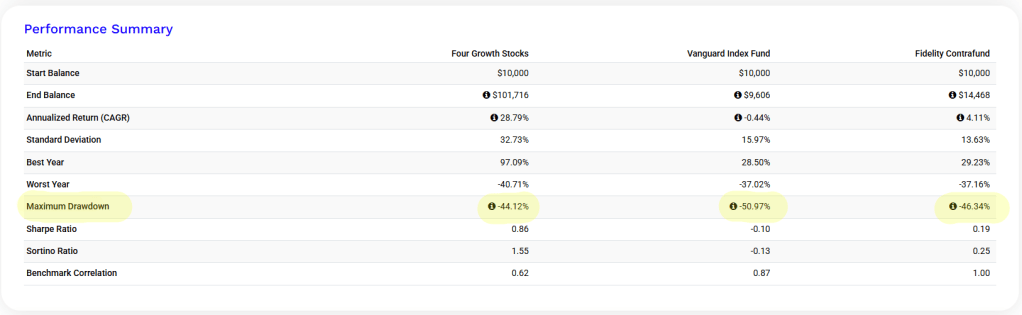

There were companies that did well in the 2000s, but not enough to compensate for the hundreds of stocks pulling the index down in those years. The investors who avoided the index as a whole and concentrated their assets in the companies that were growing in those years did very well. I found four well-known names that did generate growth for investors, whereas the index investor sat that decade out. I need you to know that just because these companies performed well 20 years ago, there’s no reason to believe that means they should do well today. This is in no way a recommendation to invest in a company that used to perform well. I’m just using these to illustrate my point. And I also need you to know that I absolutely recommend diversifying your investment portfolio well beyond just four stocks. I only used four stocks in this example because it was difficult to find many names you would recognize today that were publicly traded during that entire decade. A lot of today’s well-known companies went public during that decade, like Google, Netflix, and Salesforce, but the four companies I identified that performed well between the years 2000 and 2010 and were publicly traded the entire time were Apple, Amazon, eBay, and Lowe’s. So, I combined them into a portfolio of equal parts and back-tested it against the performance of the Vanguard 500 index fund. The concentrated growth portfolio grew tenfold over that decade. The index fund lost money. I also threw in one of the biggest mutual funds of that era, the Fidelity Contrafund, for safe measure. I don’t know how many holdings it kept in that decade, but I do know today it’s holding around 450 companies. It may as well be an index fund, and that may be why its performance mirrored the index fund over that decade.

Now, the road to 10x was a bumpy ride, but it was a ride that gained considerable elevation. You might expect the immense diversification of the index fund to have offered more stability, but of these strategies, the index fund suffered the greatest drawdown in the 2008 financial crisis.

I’m not saying index investors should expect this as their fate anytime soon. We don’t know what the future holds. And I’m not claiming credit for building such an outperforming stock portfolio back then. I wasn’t constructing portfolio models in the year 2000; I was in college. But I am constructing portfolio models now, and I built the Mainsail Equity Portfolio Model with this same sentiment in mind. When the market becomes flat, I want to have a better strategy than helplessly waiting for growth opportunities to return; I want to waste no time. I want to continuously study the market and analyze stocks to consistently seek growth opportunities, and when I find them, I want to concentrate my investors’ assets in those holdings. 15, holdings to be exact, in our current allocation. I’ve been investing in this model for a long time, and in 2025, the Mainsail Equity Portfolio Model became available to investors through Northshore Wealth Management.

I learned how to invest from Warren Buffett, but I learned how to advise people by following the integrity of the fiduciary standard that asks us to do what’s in the investor’s best interest. I believe it’s not in your best interest to resign yourselves to helplessness or risk the potential for lost decades. Learn how to invest in a strategy beyond helplessly hoping it’ll work out, or hire someone who has a plan.

That brings me back to how we got here. We were reviewing a chart designed to help us ease our worries over how the overall market will react to current events. But how might you feel if you were a little less helpless? How would this event feel as an investor if you knew you had more of a strategic plan than just hoping your portfolio will be ok? I can’t guarantee that analyzing and strategically selecting stocks that are poised for healthy growth, regardless of economic shifts or political disruptions, will result in growth over the next decade, but it sure makes more sense to me than helplessly drifting in the open waters, wondering whether you’ll make it somewhere or sink. If you study Warren Buffett’s work, you’ll see that drifting helplessly was never his strategy.