Today’s market conditions remind me of an excerpt from a writing project I’m working on in my spare time. It’s a true story and a lesson to learn from someone I’ve worked toward helping in the past. I always change names when I write about real people, so we’ll call him Ben. I wrote this in 2022.

“Ten years ago, Ben came to my team for investment ideas for the $300,000 in his savings account. Ben was hesitant to invest in the stock market at an all-time high. He decided to wait for a better time to try to enter the market. Every time we spoke to Ben over the next decade about investing his savings, we tried to lead a horse to water, but the market was always at another all-time high, and he always feared a pullback, so the timing never felt right to him, and he never got in.

In the first quarter of 2022, the stock market experienced a correction, falling 15%. Ben probably thinks he did well by avoiding a $45,000 loss. Still, the bigger picture will show that, had he been fully invested over the last 10 years and averaged a 10% annual return, his portfolio would have compounded to a value of $778,000 by now. The recent pullback would have cost him $116,700 from that account value, but he would still have $661,300 – more than double his original investment. Because Ben chose to stay in his savings account, compounding at a rate of only 0.25%, Ben’s account today is safe from market volatility but only worth $307,584.

I couldn’t make this up. These are real numbers and real consequences of trying to time the market. What do you think your investment portfolio could be worth 10 years from now?”

The writing project I’m working on is a collection of stories of the successes and failures I’ve witnessed as an investment professional over the last 20 years. Most of the failures stemmed from people waiting too long to accept professional guidance or trying to recover financially from mistakes they made on their own. Ben’s story ties in nicely with the market volatility we’re experiencing today. It’s a good time to write about how the Buffer Approach to fundamental stock analysis provides a buffer to those who invest in the portfolios that it builds.

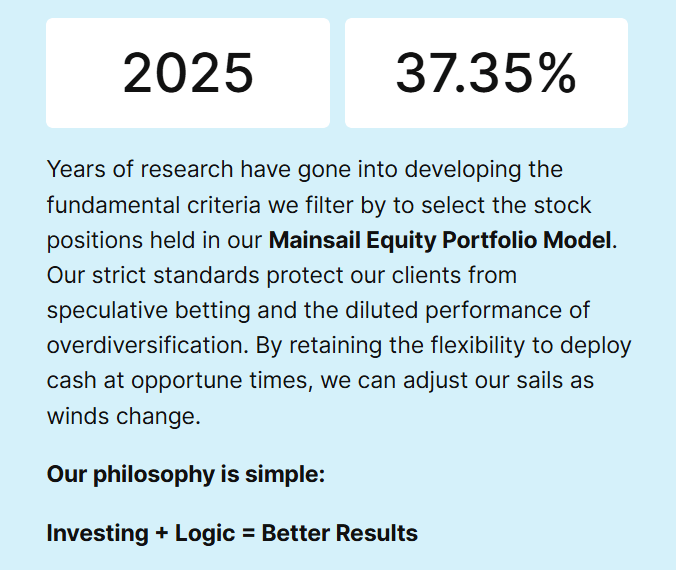

The Mainsail Equity Portfolio Model, constructed on a strong foundation using the Buffer Approach, is down 2% year-to-date (as of March 3rd, 2026). But after a 37% return last year, we have built a nice buffer of established gains that enables us to absorb some pullback and still be miles ahead of index investors and many other portfolios. But that’s not even what the Buffer Approach is named for.

The framework of the Buffer Approach provides investors with a buffer from the risk of speculation. Data-driven stock selection ensures we make decisions based on what we know, not what we hope. We don’t have to hope a company is worth investing in when we have the tools to look at that company’s finances and know for sure. Too many investors pick stocks based on assumptions or hope that it will be a good selection, and that hasn’t made logical sense to me ever since I was a kid first learning about the stock market. I worked in a candy store as a teenager, and before I went off to college, my boss wanted me to consider business as an area of study, so he gave me a brief education on the simple rules of increasing revenue and decreasing costs to run a successful business.

At the same time, I was being introduced to the stock market and reading about how the average investor pays little to no attention to a company’s financial health before they jump into buying shares on nothing but a hope and a prayer that the share price will go up. It seemed pretty cut and dry to me that you didn’t have to hope for things like this; you could just do the research and simply know whether the company was following the simple rules of running a successful business: increasing revenue and decreasing costs. I mean, there was no guarantee, but you could really narrow the odds down considerably with that knowledge alone.

It all seemed very straightforward to me, as a kid, so I started on the path that led me here, decades later, offering the benefits of analyzing these same simple business principles to investors seeking protection from how scary it is to drift in the open waters of the stock market without a life jacket, hoping your boat doesn’t sink. My guidance and experience can offer you a buffer. Over the decades, I’ve built upon the basic rules of business analysis that I learned as a kid, and I began to incorporate other measures like operating margins, price valuations, and earnings dilution, among other metrics. I can’t protect anyone from loss; no one can. But I can protect you from the risk of drifting into dangerous waters if you don’t know how to navigate.

Elevated investor sentiment has driven some asset managers to forget some of the reasons fundamental stock analysis should be the foundation of their research. My hope is that the results we’ve achieved through our research will bring others back to a more grounded philosophy in portfolio construction. I’ve been a student of the stock market since the late 1990s, and I have spent years applying the problem-solving approach of reasoning from first principles toward developing the unique application of stock analysis that is:

The Buffer Approach

Bottom-Up Fundamental Ratio Relativity (BUFRR) is an investment approach that evaluates individual companies based on their unique financial metrics compared to their own historical performance or direct peers, rather than focusing on broad macroeconomic trends. This “relativity” aspect helps determine if a stock is truly cheap or expensive based on its internal strength and competitive position, rather than just its nominal price.

Key Concepts of Bottom-Up Fundamental Analysis

- Company-First Approach: Unlike top-down analysis, which starts with the economy and looks for sectors of the market that should shine in current economic conditions, bottom-up investors look first at individual company metrics to determine intrinsic value, regardless of sector.

- Key Metrics (Fundamental Ratios): We analyze financial statements for revenue growth, profit margins, debt levels, and cash flows to identify undervalued, high-potential companies. Unique to the Buffer Approach, our “relativity” in valuation prioritizes internal analysis by measuring a company’s ratios against each other to calculate potential growth trajectories or weaknesses.

- Ignoring Macro Noise: This approach assumes a high-quality company can perform well regardless of the broader economic environment, or it is used to identify stocks with the greatest potential to perform well despite potential economic headwinds.

Advantages of These Applications

- Identifying Undervalued Opportunities: It helps identify companies that are temporarily overlooked by the market but have strong fundamentals.

- Identifying Risk: Measuring price ratios relative to overall company performance helps identify and avoid overvalued positions.

- Broad Sector Rotation: You can find opportunities in places you may not have otherwise been looking.

- Long-Term Focus: This approach is well-suited for long-term investors aiming for sustainable growth.

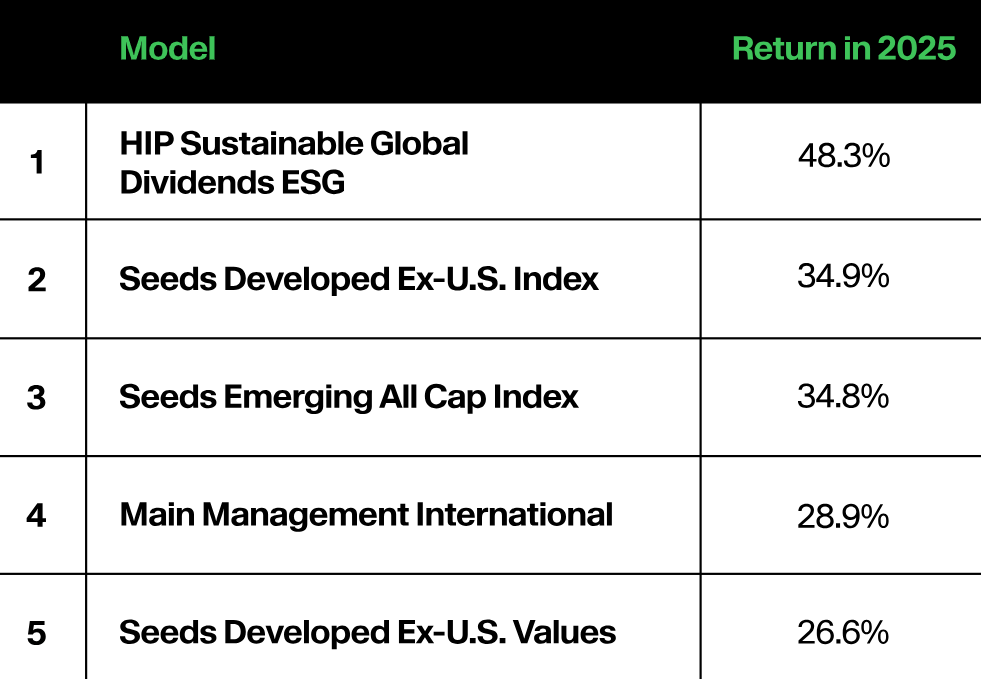

The Buffer Approach to fundamental stock analysis is used to guide portfolio construction at Northshore Wealth Management, and I let the results speak for themselves. I’ve studied market trends and capitalized on them for over two decades, and by drawing on that experience, I’ve built Northshore Wealth Management’s flagship portfolio model, The Mainsail Equity Model. When market winds change, we adjust our sails to stay on course.

Portfolios managed at Northshore Wealth Management are held on a robust brokerage platform called Altruist Financial. While the Mainsail Equity Model is available exclusively at Northshore Wealth Management, I can compare its performance with the 508 other portfolio models available on the Altruist platform, offered by 28 other asset managers. I’m proud to share that, in 2025, the Mainsail Equity Portfolio Model outperformed all but one of those competitors. Our Flagship Portfolio Model’s performance came in 2nd place out of the 509 models available to our investors.

These figures are shown net of underlying model fees and expenses. Past performance is not indicative of future results.

To be fair, some of those models are comparing apples to apples, but not all models are designed to maximize growth opportunities while managing risk quite like the Mainsail is. Some models are more heavily allocated in bonds to offer asset preservation strategies to more conservative investors.

Of course, when even one portfolio model outperforms ours, we research them to learn as much as we can from them to ensure we remain one of the top-performing asset managers in the business. I have colleagues in my industry advising me against advertising a return as high as 37%, out of fear it will scare some investors away. People either won’t trust that it’s true or they won’t trust that it’s safe. Maybe my colleagues are right, but there are investors who do value these returns and the work that goes into achieving them, and that’s who I do this work for. If doing the research to maximize potential returns and applying a buffer to shield us from senseless speculative betting sounds like a route you’re uncomfortable taking, I can’t make you. I will still be here a decade from now if it takes that long to build trust. Just remember where Ben was after a decade. I will sail onward toward our destination regardless. I know these waters, and I built this boat to sail them. Reach out if you’d like a guided tour or a boarding ticket to sail with us.